En el primer trimestre de 2026, la guerra entre Estados Unidos, Israel e Irak impactó rápidamente la sostenibilidad de las cadenas de suministro globales. Las interrupciones en el transporte marítimo a través del estrecho de Ormuz, sumadas a los daños a la infraestructura energética, provocaron un aumento significativo en los precios internacionales del petróleo y los costos de envío, que se extendió globalmente a lo largo de la cadena de "energía, logística, materias primas y manufactura", generando inflación importada y presiones de contracción de la producción.

China, como la mayor nación manufacturera e importadora de energía del mundo, se vio directamente afectada. Por un lado, la contracción de la oferta en Oriente Medio elevó los costos de los productos industriales y redujo las ganancias de las empresas; por otro lado, la escasez de materias primas petroquímicas, la inestabilidad en el suministro de materiales clave y las interrupciones en el tránsito logístico provocaron recortes de producción e interrupciones en el suministro en industrias como la química y la automotriz. Simultáneamente, las interrupciones en los centros de transporte marítimo y aéreo de Oriente Medio obstaculizaron los vínculos comerciales y de inversión entre China y Oriente Medio. Los precios internacionales del petróleo continuaron su fuerte ascenso, y los contratos de futuros de crudo nacionales también se fortalecieron significativamente. Las Naciones Unidas y la comunidad internacional condenaron enérgicamente las acciones militares unilaterales de Estados Unidos e Israel, e instaron urgentemente a todas las partes a cesar el fuego de inmediato y retomar las negociaciones diplomáticas para evitar un deterioro total de la situación. Si bien la OPEP+ está estudiando posibles planes de aumento de la producción, mantiene sus recortes de producción actuales. Es poco probable que los aumentos de capacidad a corto plazo compensen el déficit de suministro de crudo en Oriente Medio. Las primas de riesgo geopolítico siguen siendo elevadas, lo que conlleva un aumento significativo de la volatilidad de los precios en el sector energético y químico mundial.

Irán es un nodo clave en la cadena de suministro global de materias primas energéticas y una fuente fundamental de las importaciones de petróleo crudo y materias primas energéticas de mi país. Su posición geopolítica determina directamente el equilibrio global de la oferta y la demanda, así como las tendencias de precios de la energía y sus derivados. Su valor estratégico fundamental se refleja en dos dimensiones: A nivel global: En 2025, se proyecta que la producción de petróleo crudo de Irán alcance los 3,3 millones de barriles diarios, lo que representa el 3,3% de la producción mundial, y sus exportaciones marítimas representan el 4% del comercio marítimo mundial. En 2025, se proyecta que sus exportaciones de GLP alcancen aproximadamente los 10 millones de toneladas, lo que representa el 7% del comercio mundial de GLP, convirtiéndolo en el cuarto mayor exportador mundial de GLP. Su producción de gas natural representa el 6,4% de la producción mundial, lo que lo convierte en el tercer mayor productor mundial de gas natural, después de Estados Unidos y Rusia. Simultáneamente, Oriente Medio controla el estrecho de Ormuz, una vía marítima vital para el 20 %-25 % del comercio mundial de petróleo crudo por vía marítima, el 30 % del comercio de GLP y el 20 % del comercio de GNL. Las exportaciones de energía de países del Golfo Pérsico como Arabia Saudita e Irak dependen de esta vía marítima, y su paso seguro repercute directamente en la estabilidad de la cadena de suministro energético mundial.

A nivel chino: En 2024-2025, mi país importó 1,38 millones de barriles de petróleo crudo diarios de Irán, lo que representó el 13,4% del total de las importaciones marítimas de petróleo. Más del 80% de las exportaciones de petróleo crudo de Irán se dirigen a mi país. Su GLP, mineral de hierro y mineral de cobre abastecen continuamente a las industrias química, siderúrgica y de metales no ferrosos de mi país. Las industrias de metanol, MTO y PX en el sur y el este de China dependen en gran medida de las materias primas de petróleo y gas iraníes a bajo precio, lo que influye directamente en los centros de costos y las tendencias de precios de los productos nacionales relacionados.

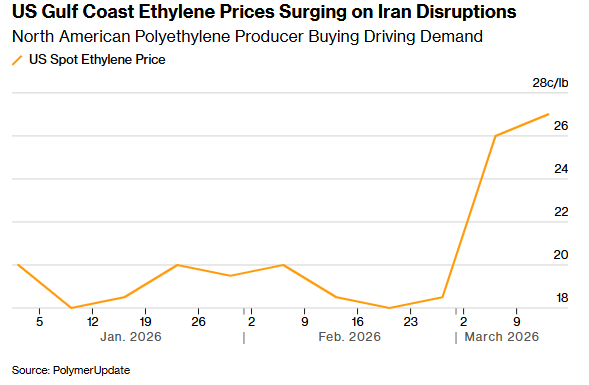

Como principal proveedor de polietileno y otros productos petroquímicos, las interrupciones en las exportaciones de Oriente Medio a través del estrecho de Ormuz han provocado una escasez de suministro mundial. Al mismo tiempo, las paradas de producción y la escasez de materias primas en Asia también han elevado los precios en toda la cadena de la industria del plástico. Monómero de acetato de vinilo (VAM)Esta dinámica está impulsando la demanda de polietileno producido en Estados Unidos. Los productores estadounidenses de polietileno están aumentando sus compras de etileno, una materia prima clave, lo que indica que los fabricantes se esfuerzan por aprovechar las oportunidades de exportación ante la escasez de suministro global.

Los precios del etileno a lo largo de la costa del Golfo de Estados Unidos también están subiendo a medida que los fabricantes acumulan materias primas. El miércoles, en el centro de Montpellier Bellevue en Texas, el etileno al contado se cotizaba a 30,25 centavos por libra. Este precio subió aún más desde los aproximadamente 27 centavos del lunes, que ya había alcanzado un máximo de un año. El aumento en los precios del etileno, una materia prima fundamental para el proceso de producción basado en etileno, ha impulsado al alza los precios del acetato de vinilo, PVA y otros productos relacionados. Jiangsu ElephChem Holding Limited, con una planta de 130.000 toneladas Alcohol polivinílico (PVA) La capacidad de producción que utiliza el proceso de carburo de calcio-acetileno tiene un amplio suministro de materia prima y precios relativamente estables, lo que lleva a una mayor diferencia de precios. La capacidad de producción de PVA en el extranjero se basa principalmente en el proceso de etileno derivado del petróleo, lo que la hace altamente susceptible al suministro y los precios del etileno; sin embargo, alcohol polivinílico de China Se prevé que aumente la demanda de exportaciones.

Sitio web: www.elephchem.com

WhatsApp: (+)86 13851435272

Correo electrónico: admin@elephchem.com

Soporta red IPv6

Soporta red IPv6